All Categories

Featured

Table of Contents

[/image][=video]

[/video]

Multi-year guaranteed annuities, also understood as MYGAs, are taken care of annuities that lock in a stable rate of interest for a specified time duration. Give up durations typically last 3 to 10 years. Because MYGA prices transform daily, RetireGuide and its partners update the following tables listed below frequently. It is necessary to check back for the most current info.

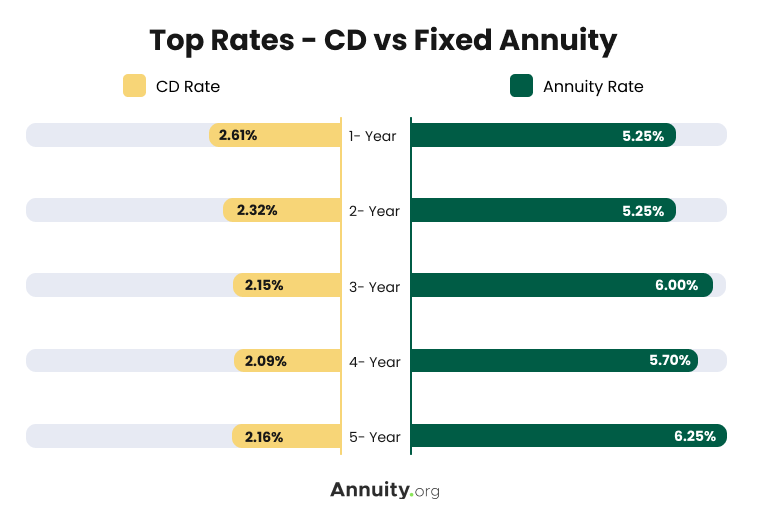

Numerous factors identify the rate you'll get on an annuity. Annuity rates often tend to be higher when the basic level of all rates of interest is greater. When purchasing taken care of annuity rates, you could find it valuable to contrast prices to deposit slips (CDs), one more popular alternative for risk-free, reputable growth.

In basic, set annuity prices surpass the rates for CDs of a similar term. Other than gaining a greater price, a dealt with annuity may offer better returns than a CD since annuities have the benefit of tax-deferred growth. This implies you won't pay tax obligations on the passion earned till you begin getting payments from the annuity, unlike CD passion, which is counted as gross income each year it's gained.

This led numerous professionals to believe that the Fed would certainly decrease prices in 2024. Nevertheless, at a plan discussion forum in April 2024, Federal Book chair Jerome Powell recommended that prices may not come down for a long time. Powell stated that the Fed isn't sure when rate of interest rate cuts could happen, as rising cost of living has yet to be up to the Fed's standard of 2%.

Pros And Cons Of Annuities Motley Fool

Bear in mind that the ideal annuity rates today might be different tomorrow. It is necessary to contact insurance policy business to validate their details prices. Beginning with a free annuity consultation to find out how annuities can help money your retirement.: Clicking will take you to our companion Annuity.org. When contrasting annuity prices, it is essential to perform your very own research study and not exclusively choose an annuity just for its high price.

Think about the type of annuity. A 4-year set annuity could have a greater rate than a 10-year multi-year assured annuity (MYGA).

The warranty on an annuity is just just as good as the company that issues it. If the firm you buy your annuity from goes damaged or bust, you could shed money. Examine a company's economic toughness by consulting across the country identified objective rating firms, like AM Ideal. A lot of experts suggest just thinking about insurance providers with a rating of A- or over for long-lasting annuities.

Annuity revenue climbs with the age of the purchaser since the revenue will be paid out in less years, according to the Social Protection Administration. Do not be stunned if your price is greater or less than a person else's, also if it coincides product. Annuity prices are simply one aspect to take into consideration when buying an annuity.

Comprehend the fees you'll have to pay to administer your annuity and if you need to cash it out. Cashing out can cost approximately 10% of the worth of your annuity, according to the Wisconsin Office of the Commissioner of Insurance coverage. On the other hand, administrative fees can accumulate with time.

Colorado Bankers Life Annuity

Rising cost of living Inflation can consume up your annuity's value over time. You can think about an inflation-adjusted annuity that increases the payouts over time.

Check today's listings of the ideal Multi-year Surefire Annuities - MYGAs (upgraded Thursday, 2025-03-06). These listings are arranged by the abandonment cost duration. We modify these listings daily and there are constant modifications. Please bookmark this web page and return to it typically. For specialist assist with multi-year ensured annuities call 800-872-6684 or click a 'Get My Quote' switch beside any type of annuity in these checklists.

Delayed annuities permit an amount to be withdrawn penalty-free. Deferred annuities typically allow either penalty-free withdrawals of your made rate of interest, or penalty-free withdrawals of 10% of your agreement value each year.

The earlier in the annuity period, the higher the fine portion, referred to as surrender charges. That's one reason that it's ideal to stick with the annuity, once you devote to it. You can take out every little thing to reinvest it, yet before you do, see to it that you'll still come out on top this way, even after you figure in the abandonment cost.

The surrender cost might be as high as 10% if you surrender your agreement in the very first year. Usually, the surrender charge will certainly decline by 1% each contract year. An abandonment fee would be credited any kind of withdrawal above the penalty-free quantity allowed by your deferred annuity contract. With some MYGAs, you can make very early withdrawals for emergencies, such as health and wellness expenditures for a severe illness, or confinement to an assisted living facility.

When you do, it's best to persevere to the end. First, you can set up "systematic withdrawals" from your annuity. This means that the insurer will send you repayments of passion monthly, quarterly or yearly. Utilizing this method will certainly not take advantage of your original principal. Your other alternative is to "annuitize" your delayed annuity.

How To Get Money Out Of An Annuity

This opens a selection of payout options, such as earnings over a solitary lifetime, joint lifetime, or for a specified period of years. Many deferred annuities enable you to annuitize your agreement after the initial contract year. A major difference is in the tax treatment of these products. Rate of interest earned on CDs is taxed at the end of yearly (unless the CD is held within tax obligation qualified account like an IRA).

Likewise, the interest is not strained up until it is removed from the annuity. Simply put, your annuity expands tax obligation deferred and the rate of interest is compounded annually. However, window shopping is constantly an excellent concept. It holds true that CDs are guaranteed by the FDIC. MYGAs are guaranteed by the individual states normally, in the range of $100,000 to $500,000.

Athene Annuity And Life Assurance Company

You have several options. Either you take your money in a lump amount, reinvest it in one more annuity, or you can annuitize your agreement, converting the round figure right into a stream of revenue. By annuitizing, you will only pay taxes on the passion you receive in each settlement. You have 30 days to inform the insurance firm of your objectives.

These functions can differ from company-to-company, so be certain to discover your annuity's survivor benefit attributes. There are numerous benefits. 1. A MYGA can mean lower taxes than a CD. With a CD, the rate of interest you gain is taxable when you make it, although you do not get it until the CD develops.

So at least, you pay tax obligations later, as opposed to faster. Not just that, yet the worsening interest will certainly be based upon an amount that has not currently been tired. 2. Your beneficiaries will certainly obtain the full account value as of the day you dieand no surrender charges will be subtracted.

Your beneficiaries can select either to receive the payout in a lump sum, or in a series of revenue settlements. 3. Commonly, when someone dies, even if he left a will, a court chooses that gets what from the estate as sometimes family members will certainly suggest concerning what the will certainly ways.

It can be a long, made complex, and very expensive process. Individuals most likely to wonderful lengths to prevent it. With a multi-year fixed annuity, the owner has actually plainly assigned a recipient, so no probate is required. The cash goes directly to the recipient, no doubt asked. If you add to an IRA or a 401(k) strategy, you obtain tax obligation deferment on the profits, much like a MYGA.

{kind=link}

Latest Posts

5 Year Deferral Inherited Annuity

Bonus Rate Annuity

Krause Financial Medicaid Annuity